London is still the number one city in Europe for cross‑border real estate investment in 2026, according to CBRE’s European Investor Intentions Survey 2026. However, the big story for this year is the rise of the chasing pack; Warsaw and Madrid have now climbed into the top three most favoured destinations for international capital, outperforming traditional heavyweights and sitting alongside Barcelona and Milan in a new elite tier of European growth markets.

What is the CBRE European Investor Intentions Survey 2026?

CBRE’s European Investor Intentions Survey 2026 is based on answers from nearly 700 investors. It looks at where they plan to put money in European real estate this year and which sectors they prefer. One key point is that for the most attractive markets section, CBRE only counts answers where investors picked a location outside their own country. This gives a clear picture of cross‑border interest rather than domestic bias. The survey shows which European countries and cities investors favour for 2026, how confident they feel about buying, and which sectors they prefer, such as Living, Logistics, Office, and Retail. For anyone deciding where to focus in 2026, it is a useful sense‑check against what the wider market is thinking.

Top European investment cities in 2026: London leads, Warsaw and Madrid surge

London remains the leading city for cross‑border investment. CBRE’s survey confirms that London is still the top European city for cross‑border real estate investment in 2026. That should not shock anyone, but it matters. Investors keep backing London because it has deep, liquid markets across most asset types and a long track record of international capital entering and exiting. The legal and lending frameworks are familiar to global investors. If you want scale, deal flow, and a market you can explain to your investment committee in one slide, London is still the default pick.

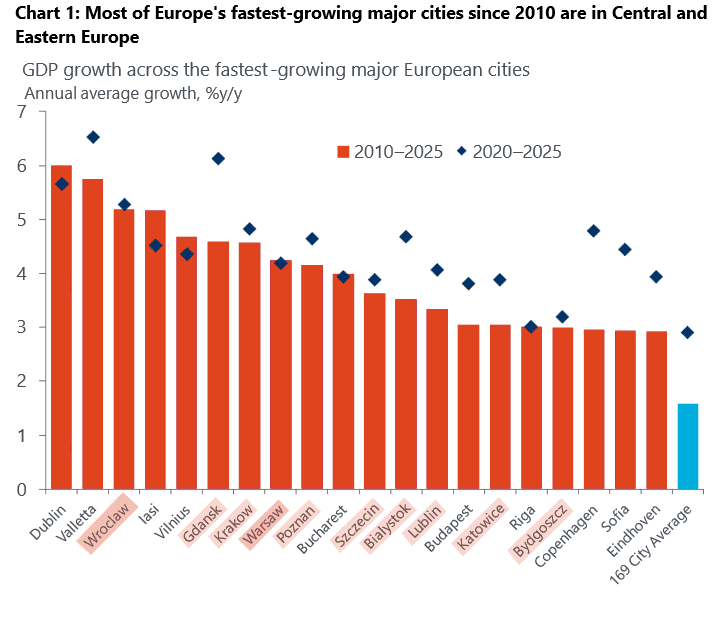

Warsaw and Madrid are no longer just also‑rans; they are now in the clear front rank. The public summary of the survey groups Madrid, Warsaw, Barcelona, and Milan as cities that rank closely behind London. That makes it sound like one neat group, but in practice, Warsaw and Madrid deserve separate attention as they lead this secondary tier. From the survey, Spain is the top country at the European level, and Madrid is one of the key cities driving that position. Warsaw holds its place as a leading Central and Eastern European market with sustained investor interest. Madrid benefits from strong demand in key sectors and a supportive macro backdrop, while Warsaw benefits from solid economic performance and investor comfort with CEE risk. If you are still thinking of Warsaw as a niche play, you are behind the curve.

Barcelona and Milan are still very much in the race. CBRE’s summary also highlights Barcelona and Milan as ranking closely behind London. They are not side notes. Both cities offer scale in their national markets and a base of domestic and international tenants. They have clear roles inside their wider regions, particularly in Southern Europe. Together, Madrid, Warsaw, Barcelona, and Milan form the next tier of cross‑border targets, each with its own story and risk profile.

Why Poland and Spain are leading the 2026 outlook

One of the more striking survey findings is that Spain moves into the top position at the country level. CBRE links this to resilient macro fundamentals and broad demand across major sectors. For investors, this means Spain is not a single‑city bet; interest extends across several markets. Madrid and Barcelona are the obvious entry points, but there is clear comfort with Spain as a whole. If your current allocations still treat Spain as a side allocation, the survey suggests it is time to revisit that stance.

The survey also notes that select CEE locations hold their position, and Warsaw is the stand‑out city in that group. Reasons investors stick with Warsaw include stable economic performance compared with parts of wider Europe and a growing occupier base across sectors. There is a clear history of cross‑border capital into offices, logistics, and living assets. It is not a fringe pick. For many investors who want yield and growth without going into far smaller markets, Warsaw is the logical CEE choice. You can read more about our specific Warsaw market analysis to see how these trends play out on the ground.

Investor confidence in 2026: 89% expect buying to increase or hold steady

A key line in the CBRE summary is that 89% of respondents expect purchasing activity to increase or remain steady in 2026. After a period of uncertainty and poor price discovery in some segments, there is a clear shift in tone. This matters because more trades usually mean clearer price signals,s and buyers and sellers start to agree on value again. Investors can move from watching to actually deploying capital. This improvement in confidence is backed by a more stable macro backdrop, lower debt costs than in the worst of the rate shock, and better clarity on valuations across sectors. If you have been sitting on dry powder, 2026 is shaping up as a year where you either move or find yourself chasing sharper pricing later.

CBRE’s survey suggests that most investor profiles plan to keep or increase their real estate allocations in Europe. General partners show strong intent to deploy capital, helped by higher levels of capital raised in 2025. This capital now needs to be placed. Investors still see value in core‑plus and value‑add plays, and core interest has picked up year‑on‑year as rental growth expectations firm up. In London, that may mean more competition for core assets, while in Warsaw and Madrid, core‑plus and value‑add may still offer entry points with headroom. If you plan to wait for the bottom, you may find the market has already moved on.

Sector outlook: Living and Logistics still lead

For the second year in a row, the Living sector is the most preferred in CBRE’s European investor survey. Key drivers include structural supply gaps in many cities and steady occupier demand. In London, well‑located living stock continues to attract global capital, while in Warsaw and Madrid, demand growth and supply limits can support rental growth. Logistics remains a leading choice alongside Living. Investors like logistics because trading liquidity has built up over the last decade, and occupational demand is still firm. In 2026, the smarter logistics plays are likely to be well‑connected urban or near‑urban assets.

CBRE notes that sentiment towards Office and Retail has improved year‑on‑year. That does not mean every office or retail asset is suddenly back in favour, but it does mean more investors see selective opportunities. Repriced assets with solid cash flow and realistic capex plans get a fair hearing. In London, high‑quality, well‑located offices will stay the natural cross‑border focus, while in Warsaw and Madrid, a mix of repriced assets and growth stories can stand out. Retail remains very stock‑specific, but the worst of the mood music has faded.

How to use the report for your own strategy

London at the top, followed by a group of Warsaw, Madrid, Barcelona, and Milan, gives a clear picture of where cross‑border capital is most comfortable. But the right city for you depends on your hold period, risk appetite, and sector focus. Shorter holds favour deeper markets like London, while a higher yield or growth focus may tilt you towards Warsaw or Madrid. Use the list as a guide rather than a must‑buy order.

To turn these insights into action, you should start by picking your main sectors and matching them to the cities that fit your mandate. Check the liquidity and exit routes to make sure there is enough depth in the segment you want inside that city. Finally, pressure‑test the findings against your house view. If you are looking for a partner to help you identify the best opportunities in these high‑growth markets, you can contact the Varso Invest team for a detailed consultation.

No survey result is a guarantee, and there are risks to keep in mind for 2026. Financing conditions can change again if inflation or rates move in the wrong direction, and pricing alignment can slip if sellers anchor to past values. Geopolitical noise can also affect cross‑border flows. The safest way to use the CBRE findings is as one input in your decision set, backed up by local leasing data and your own risk framework. You can download the full report from the CBRE website to see the complete market‑level detail.